Gas bulls sweat it out

Searing temperatures in Asia and LNG supply disruptions buoy EU gas prices. But for how long? | EU LNG Chart Deck 29 Apr-10 May 2024

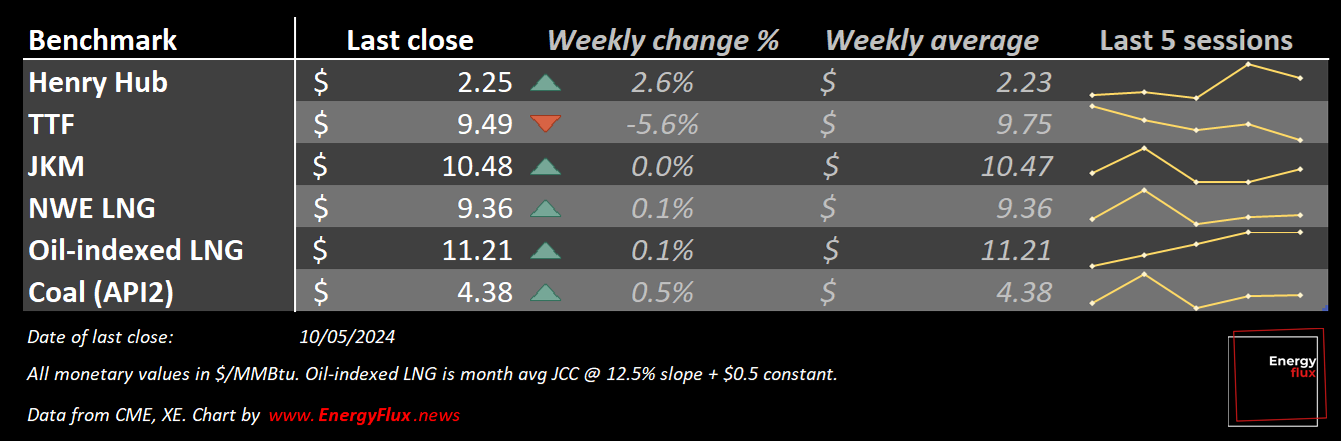

Bullish sentiment is breaking out across global natural gas markets. Whether you put it down to market fundamentals or market manipulation, the fact remains that traders are bidding up near-term prices in Europe and Asia. But the outer reaches of the forward curve tell a very different story.

Let’s take a quick look at the fundamentals underpinning the bullish thesis. The global supply-balance has tightened somewhat thanks to a big drop in US liquefaction rates and a major outage at the Gorgon LNG project in Australia that could last well into the northern hemisphere summer.

Simultaneously, sweltering temperatures are driving demand for gas-fired power to run air conditioning units in major Asian economies. This has necessitated a higher spot price to pull LNG cargoes out of the Atlantic, stimulating a price response from traders in Europe with an eye on the gas restocking task ahead.

Hedge funds are now piling into futures markets on the expectation that this upward momentum will endure over the coming months.

It matters not that European gas stocks are still at the very highest end of the 2015-2020 seasonal norm for this time of year, nor that Europe’s ‘recovery’ in industrial gas demand — such that it is — was more than offset by lower heating and power sector gas demand in Q1’24.

Nor does it seem to matter that temporary LNG supply disruptions over the first quarter period are just that — temporary. US LNG feed gas volumes are already picking up again after a sharp downturn over December-April, and Gorgon won’t stay offline forever.

So, how should we reconcile the bullish price narrative with facts on the ground? This week’s EU LNG Chart Deck seeks to do just that, with the usual smorgasbord of original Energy Flux charts visualising prompt and forward prices, inter-basin differentials, calendar spreads and much more.

Let’s jump in.